When disaster hits, stress rises even faster than water from a flood or smoke from a fire. For homeowners and business owners, property loss is only the beginning. The insurance claim process that follows can often feel just as overwhelming. Knowing the right moves will help you secure the payout you deserve, whether the cause is a fire, flood, or windstorm. This guide gives real insurance claim tips, describes what really happens behind the scenes, and provides actionable ways to maximize every dollar in your claim after disaster strikes.

Immediate Response After a Disaster Event

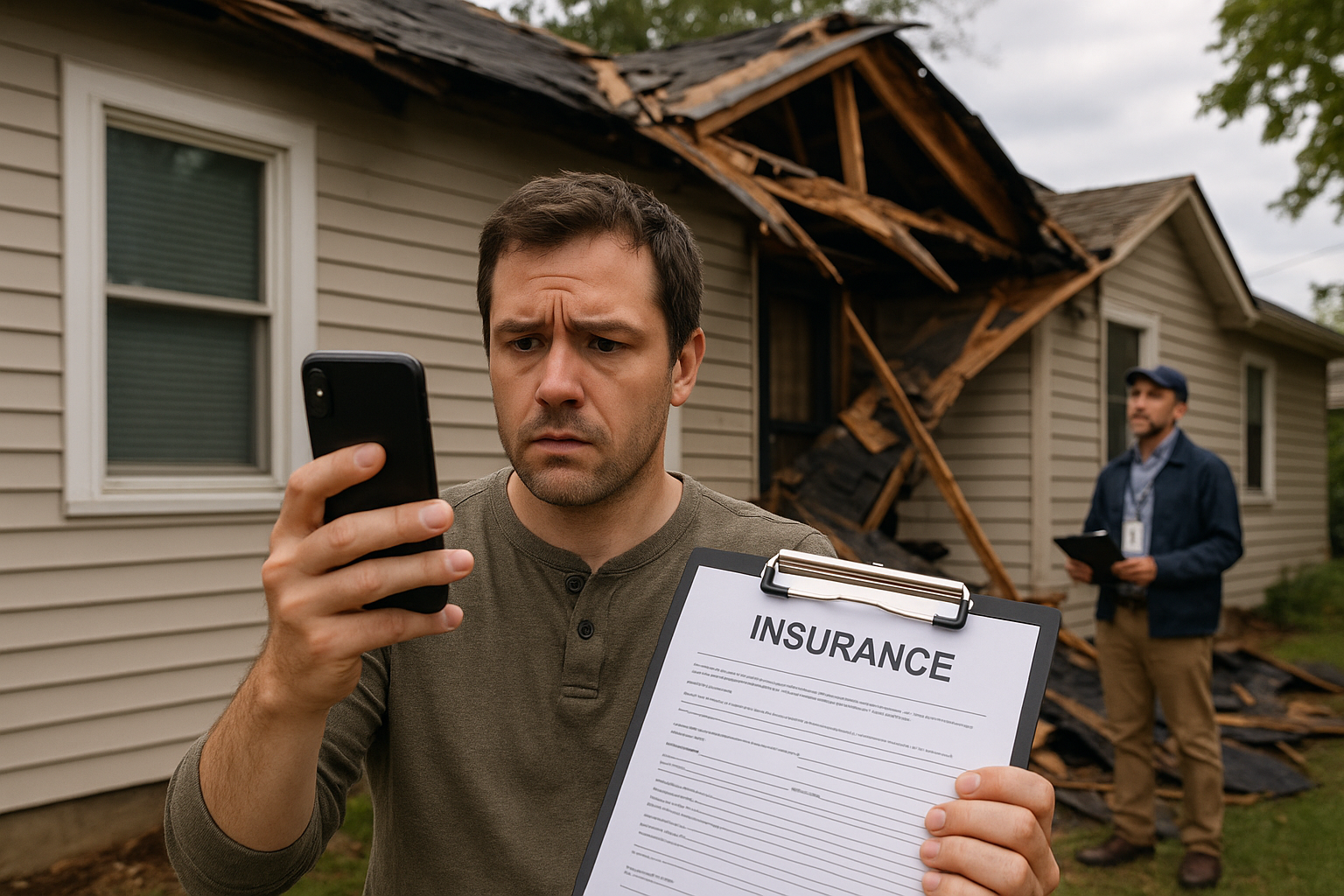

After a disaster, timing shapes everything. Contact your insurance company as soon as it is safe. Report your loss promptly. Most insurers have 24-hour claim hotlines or online reporting options. This quick start moves your claim forward while the event is fresh in both your mind and the insurer’s. The sooner you act, the sooner an adjuster gets assigned, and the faster your claim can get reviewed.

Documentation forms the backbone of any successful claim. Take photos or videos of all damage inside and outside. Cover not only big things like collapsed roofs but also smaller items that suffered water or smoke exposure. Open every closet, look under sinks, behind appliances, and inside cabinets. For ruined electronics, furniture, or personal items, keep a detailed inventory. Write down brands, models, serial numbers, and estimated values to go along with your images. The clearer the documentation, the fewer questions you face from insurance staff later on.

Act quickly on any temporary repairs that help preserve your property. Board up broken windows. Put tarps over exposed roof areas. Remove soaked carpets or furniture that might draw mold. Always save receipts for emergency materials, as your policy often reimburses these reasonable costs. Make only repairs that keep your home safe and clean, not any permanent fixes until insurance gives the green light.

Understanding What Your Policy Really Covers

Before any claim moves forward, review your insurance policy in full. This will reveal exact coverage limits, exclusions, and deductibles. Many discover only after disaster hits that certain causes, like flooding or earth movement, are not always covered by a standard homeowner’s policy. Others find out about sublimits that reduce payouts on personal property, landscaping, fences, or valuable collections.

Think through both the hundred and eighty percent rule and replacement cost. If your home is insured for less than eighty percent of its true rebuilding value, your policy might reduce a claim payout for some losses, regardless of the actual amount or formal estimate. Use online calculators or professional appraisals to re-evaluate coverage at each renewal, especially after home improvements or additions.

A common pitfall is confusing what is covered for its actual cash value versus replacement value. Replacement cost pays what it takes to buy a new item of similar kind and quality, while actual cash value subtracts for age and wear. Scrutinize terms for personal property, structural parts, and even extra living expenses should you need to move out during repairs. Being clear on these differences helps you appeal unfair reductions or underpayments later in the process.

Smart Prep Before the Adjuster’s Visit

The insurance adjuster becomes your main point of contact during the claim review. Prepare for this meeting as if you were presenting your own case in court. Organize every bit of documentation you collected right from the start, photos, videos, itemized lists, repair receipts, and a copy of your insurance policy. Write a short summary describing what happened and when. This will help the adjuster follow the story efficiently.

If possible, get repair estimates from trusted local contractors before the visit. Presenting realistic quotes frames expectations about the cost of rebuilding or replacing property. Bring up any special issues, like code upgrades required by city or county inspectors. Specific evidence gives extra support for higher repair or rebuilding costs that go beyond a simple repair job.

Keep a written log of every contact with the insurance adjuster and company representatives, noting names, dates, and what was discussed. Jot down any promises or deadlines mentioned, this can serve you well if delays or miscommunications pop up along the way. Stay present during an onsite inspection if possible, so you can point out hidden damages like warped floors, cracked foundations, or soaked subflooring that might not be obvious at first glance.

How Adjusters Evaluate Your Claim

The adjuster works for your insurance company, not for you. Their job is to assess what was lost and what it costs to replace or fix everything that the policy covers. Give them clear and complete information, this improves accuracy and leaves little room for error or lowballing.

During inspection, demonstrate affected areas and show evidence of all lost property or structural damage. Declutter the space before the adjuster arrives, as this helps them photograph damage without distractions. Share comprehensive inventories and any relevant receipts or warranties you have gathered.

If disagreements arise regarding values or the cause of loss, remain calm and provide logical supporting evidence. Note any discrepancies between the adjuster’s assessment and your repair estimates. If you feel the estimate is too low, request an itemized explanation and follow up with your own evidence. Communication and organization help settle differences without delay.

Avoid the Traps: Common Mistakes After Disaster

Beware of unlicensed contractors who often show up after disasters promising quick, cheap fixes. These operators may provide poor workmanship, disappear after taking large upfront payments, or even disappear altogether. Always check licensing, insurance, and references, and never pay the full price before any work starts. Seek recommendations from your insurer or trusted local restoration firms instead.

Do not rush to accept the very first settlement offer you receive from insurance. Press for full scope estimates and justification for any depreciated values, denied items, or partial payments. If the settlement seems rushed or unreasonable, push for re-inspection or a second adjuster. The initial offer is often negotiable, so question anything that seems incomplete or unfair.

Watch out for delayed reporting, missing documentation, or poor organization. These slip-ups drag out the process and may cause denied coverage for additional damage that happens after the disaster. Stay organized right from the beginning to reduce stress and delays during claim review.

When Extra Help Can Make a Big Difference

If you keep running into dead ends, consider hiring a licensed public adjuster. A public adjuster works as your personal advocate and negotiates directly with your insurer to help you get a fair payout. They often charge a small percentage of the settlement, but this fee can quickly pay for itself if your claim is complex or if your insurer repeatedly underpays. Choose one with local experience, a proven record, and all required credentials.

For many, insurance does not cover everything. Federal disaster programs like FEMA provide grants, low-interest loans, or emergency assistance after widespread disasters officially declared. These resources help fill gaps, cover uninsured losses, and pay for essentials like temporary housing or business operation costs during the recovery phase.

Restoration professionals often bring added value, helping document damage, prepare estimates, and handle repairs in line with insurance requirements. Some restoration companies even offer direct insurance billing and work as a go-between for you and your adjuster. This can reduce stress, speed up repairs, and improve claim accuracy from start to finish. Be sure to work with restoration firms endorsed by the Better Business Bureau and with a proven local track record, such as BORA Restoration.

Straightforward Steps to Improve Your Insurance Claim

Staying proactive from day one improves results at every stage of the disaster insurance process. Quick reporting, detailed documentation, and a methodical approach lay the groundwork for a smooth, fair payout. Always read policy language with care and check coverage gaps before renewal. Ask questions when anything seems unclear, both with your insurer and with independent restoration or insurance professionals.

Keep every receipt, communications log, and a running record of how your claim progresses. Follow deadlines issued by your policy, state law, or your insurer’s internal guidelines. Do not let temporary repairs or living costs pile up without written authorization if your policy restricts how much can be spent. When in doubt, consult with a knowledgeable adjuster, attorney, or trusted local restoration expert before making decisions that might affect your ultimate payout.

Use trusted digital tools or apps to track your claim. Many insurers allow you to upload photos, receipts, and loss inventories from your phone or desktop. Technology streamlines communication with your adjuster and creates a reliable backup in case paperwork gets misplaced. Most disputes with insurance can be prevented by exchanging clear information and following proven steps every step of the way.

In the aftermath of disaster, information is your strongest defense. By applying these insurance claim tips from professionals and regulatory experts, you move out of reaction mode and start to feel in control. That means faster repairs, a safer living space, and a path to financial recovery that works for you.